We are going to discuss a company whose founder is known for his vision, analytical thinking, and taking different routes than the rest.

Management

Shilpa medicare was founded by Mr. Vishnukant C. Bhutada in 1987, having its first contract manufacturing unit in Raichur, Karnataka. Back then Ahmedabad, Mumbai, and Hyderabad were top cities for Pharma companies yet he started his unit in Raichur and did face challenges in finding manpower but the rest is history.

He was born in a Maheshwari Marwari Family and against the community trend of doing B.com and joining family Business, he decided to pursue B. Pharma and post that founded Shilpa Medicare. His family was in the business of textiles so Pharma was something different he pursued.

Although the company started with contract manufacturing, slowly they entered API (Active Pharmaceutical Ingredients) business. In 2000 when all major pharma companies were trying to focus on Cardio, Diabetes, etc. he realized based on the research that Cancer(Oncology) would be one of the major issues going forward due to the lifestyle and focused on that.

Cancer back then was dominated by select few Pharma companies having well-established R&D capacity. Having already supplying APIs for oncology, the next logical step for them was to enter in formulation business of Oncology. Once the patent expired company did vertical integration and launched Oncology generic drugs.

What's the present situation?

Today Shilpa Medicare Limited is a global brand in the manufacturing and supplying of affordable API and Formulation globally in regulated and emerging markets.

The company supplies 30 oncology Apis and a total of 44 oncology and non-oncology APIs to regulated markets and emerging markets.

Additionally, the company also offers oncology formulations, the company has 16 injectable dosage, 19 oral solid dosages, and 13 formulations under the wholly-owned subsidiary Shilpa Therapeutics Private Limited.

Let's have a look at the business focus of the company

API

Formulations

Biologics/Biosimilars

Novel Biologic

Dermatological Formulations

Oral Dissolving Films & Transdermal Products

At present, the company has its major revenue coming from API and formulations. The company is actively advancing the research and product launch in Biosimilars and Biologics. Biologics are drugs that are made from living organisms and Biosimilars are the corresponding generic version having a similar effect that can be introduced post the patent expiry.

As evident biologics and biosimilars are complex and require more R&D and expenditure as compared to the drugs made from chemicals. Biologics are advancing among the top drugs as they can cure complex diseases.

Although biosimilar is complex to make but to maintain margin, generic pharma companies need to focus on regulated markets and launching products before the rest and continue launching newer and newer products to maintain margins and lead and this is what Shilpa medicare is aspiring to do. The company has also increased R&D spending to launch biologics along with biosimilars. The company has also been focusing on Novel Biologics. The company has patents in biosimilar (only 1 in biologics and the rest are biosimilars) and they are in clinical phases and the company is hoping to launch products by the end of 2022 in biologics and Novel Biologics.

Additionally, the company is focusing on Dermatological Formulations, Oral Dissolving Films & Transdermal Products for future growth.

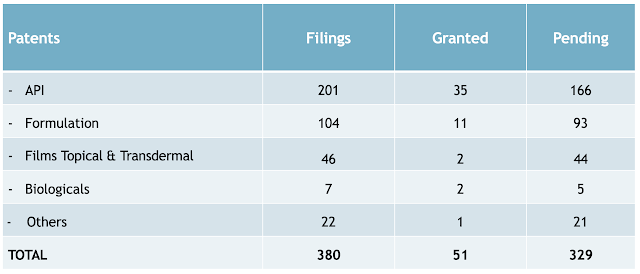

In the recent Quarter company claimed to have filed a total of 380 patents and have received grants for 51, don't confuse this with the Patents of new drugs, the majority of the patents here are for generics, and Biologics patent granted is yet to be commercialized. This also includes patents of customers as the company offers CRO, CDMO services.

The good thing here is that the company is also investing a lot in R&D and patents although majorly for generics at present but advancing in new drug patents as well.

Manufacturing and R&D centers

The company has 5 manufacturing facilities for APIs and formulation products in India and 1 manufacturing facility for APIs in Austria. The oncology formulations are manufactured in Jadcherla Unit.

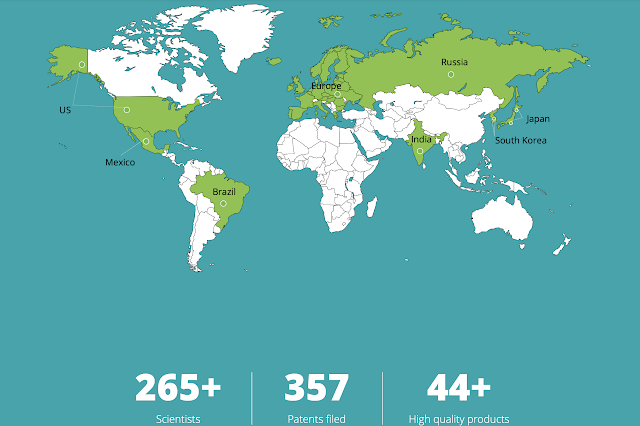

Sales Geography

As we can see the company sells its products in regulated markets like the US, Europe, Japan, Russia, South Korea, and emerging markets like Brazil, Mexico, India, etc..

India contributes 36.2% of sales(Oncology and Non-oncology), USA and Europe being regulated market contribute 44% of sales. The company is well-diversified geographically and expanding in Russia, Canada, Spain, etc..

Historical Performance

The company has performed well last year but before that performance has been subdued, revenue rose from FY16 to FY18 but fell in FY19 and had a good comeback in FY20 due to the formulation business doing exceptionally well and APIs too had good growth. A similar trend exists in bottom-line performance.

APIs have dominated the sales but as we can see formulation business had tremendous growth and the company is targeting 4x sales of formulation in FY21 YOY.

Q1 Standalone Result

Q1 sales rose 39% supported by 78% growth in formulations business and 33% growth in API business. EBITDA margin improved from 26% to 37%, bottom line PAT had 230% growth.

Recent Updates

Increased capacity of API facility for Tranexamic Acid by nearly 100%. This is the non-oncology API and sales are major to India and Europe at present.

Acquired FTF Pharma which offers integrated drug development services.

Established wholly owned subsidiaries in Canada & Spain to expand sales.

Launched 4 new products in the Oncology segment in the Indian market at affordable costs

Ibrushil

Dasashil

Axishil

Lenshil

Launched Green Tea Film, which is first of its kind and unlike the traditional green teas, the film completely dissolves and leaves no residues. The company is targeting sales of 25 crores in the first 2 years and 100cr in the next 5 years. The green tea was developed in-house and is patented.

They received a warning letter on October 8, 2020, from the USFDA for its Jadcherla facility, Telangana, and as we know that facility is used for oncology formulations and it can have major impacts on the new launches and existing oncology formulation business but management has guided minimum impact. We have to wait until Q3 results to see the clear impact of this on the formulation business. The company is actively working with USFDA to get it resolved. This news caused the stock to fall 12% in a single day and it is a big negative.

Valuations:

Currently, the stock is trading at 477 RS and with a PE of 15.4 against the industry peers of 37 but that is because the future earnings could be impacted due to USFDA warning and the company is small. The Price to book is 2.68 which is decent.

Final Verdict

The company is good and having a niche focus on Oncology with global leadership and advancing well backed by R&D and patents. USFDA warning could impact the oncology formulation earning and that would cause weakness in the stock in the short term. Valuations are not very expensive so it can be accumulated at lows for the long term, but it is always advisable to put money in multiple pharma companies instead of just one as regulatory risks always exist and one such warning can cause the stock to fall 30% or more.

Brief Background Arun Kumar, who is a common promoter for Strides Shasun and Sequent Scientific (both are listed in the market) decided to create a new company which would focus purely on APIs, as the APIs were low margin business and making it difficult to maintain margin, with this goal in mind he demerged the low margin API(Ibuprofen, Gabapentin, and Ranitidine, etc..) business of Strides Shasun and Human API business of Sequent Scientific to create SOLARA ACTIVE PHARMA, which would be a pure API company. In March 2017, the board of directors of Strides and Sequent approved the demerger, and in March 2018, the scheme got approved by NCLT and the company got listed on June 27, 2018. According to the deal, for every 6 shares held in Strides, 1 share of Solara was allotted and for every 25 shares held in Sequent, 1 share of Solara was allotted. Strides Shasun retained the formulation business and High Margin API business, and Sequent Scientific ...

Little Background Aarti Surfactants Ltd was formed after demerger with Aarti Industries. The home and personal care segment of Aarti Industries was not doing well so management decided to split it, for every 10 shares held by Aarti Industries investor they got an option of either getting one equity or redeemable preference share of Aarti Surfactants. The demerger was approved in June 2019 by NCLT and the demerged entity got listed in July 2020. Now you already know the promoters are great and they have created wealth for investors. Turnaround The company was loss-making in FY18-19, but they made a profit of 2.09 crore in FY19-20 as compared to a Net Loss of 6.47 crore in FY18-19 which implies demerger was a good call by promoters and it worked. Company Overview Aarti surfactant is one of the leading producers of ionic and non-ionic surfactants and specialty products. What are surfactants you ask? Well, surf...

Comments

Post a Comment